Summary:At present, the global essence and fragrance industry is monopolized among the leading enterprises in Europe, the United States and Japan, meeting the characteristics of diversified product layout, high R&D investment and high gross profit. Compared with overseas, the supply of essence and fragrance industry in China is relatively scattered, the market competition is fierce, and the scale of enterprises is still small. In the future, China's leading enterprises, under the external force of policy and demand changes, are expected to increase market share and replace imported products by developing high-end essence and spice products.

International market: leading monopoly, high wall casting with high gross profit margin

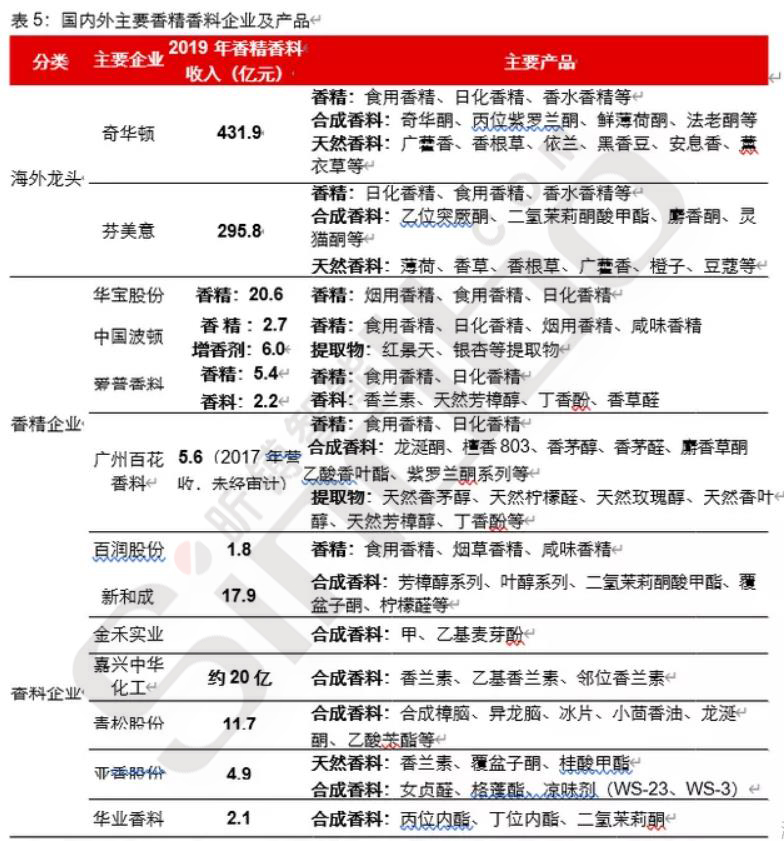

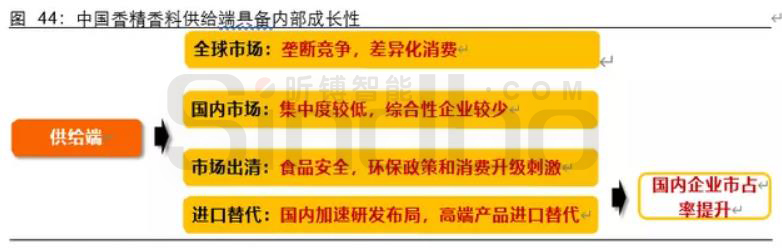

The market is highly monopolized, gradually forming a pattern of the "Four Great Kings". The global essence and spice market is monopolized by the top 10 giant enterprises. In 2017, the industry CR10 was 77.0%. With the strengthening of the layout of leading patents, the broadening of product layout, the deepening of the industry moat, and the trend of further improving market concentration. The global essence and spice market has formed a supply pattern of "four super and more powerful". Chihuadun, Fenmeiyi, International essence and Fragrance and Symrise are in the first echelon of the industry, and the second echelon is mainly Japanese, American and Chinese enterprises such as Man's, Frutarom (acquired by IFF in 2018), Takasa, Morin, Robert (owned by Fenmeiyi), Hasegawa and Huabao International.

Differentiated product competition, emphasizing the extension of consumer attributes. Since flavor products need to be blended to produce essence, different flavor products have differentiated characteristics and can form certain complementarities. The market will still pursue the production of different types of essence and spice products to pursue product renewal and meet the demand for new flavors. International essence and fragrance giants such as Chiwharton need to synthesize hundreds of new compounds every year. After the evaluation of flavor mixing personnel and synthetic process, only a few of them can be produced as new synthetic flavors. The application of these new products plays an important role in the quality of essence and the creation of new essence. Although the research and development of a single variety requires a large amount of investment, a new type of essence will gain more market space if it is applied, such as rose ether in the 1860s, turquoise ketone and turquoise ketone in the 1970s, and methyl dihydrojasmonate in the 1980s. The international essence and spice market is in the stage of differentiated competition as a whole, and even the international essence and spice giants need to purchase relevant products from competitors for blending.

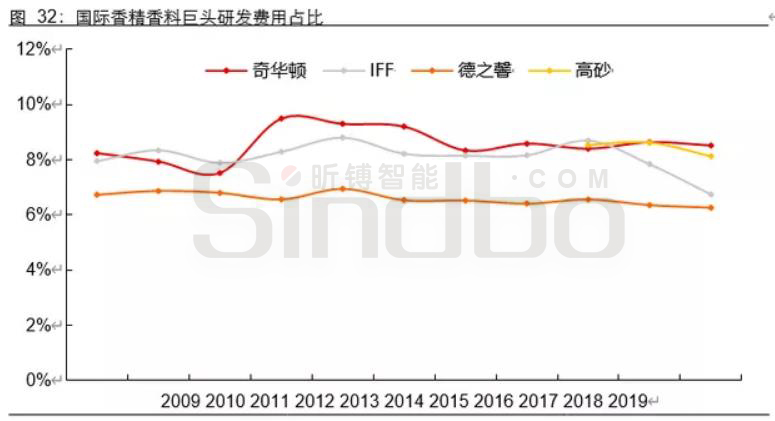

Continuous high R&D investment, consolidating the leading position. New essence and spice products can bring certain differentiation to products, improve customer stickiness and seize market share. The world essence and fragrance giants attach great importance to R&D, and the general R&D investment accounts for 6% to 9% of the total revenue. These funds are mainly used for the development of various new products and technologies, effectively promoting the development and application of related technologies. The extremely high R&D investment has created a highly competitive barrier in the industry, promoting a pattern of monopolistic competition.

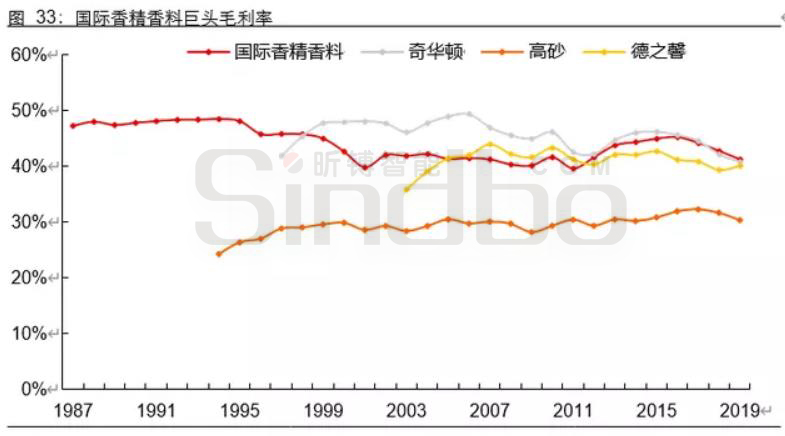

The cost proportion is relatively low, and the gross profit margin level is high. On the demand side, essence and fragrances account for a relatively low proportion of production costs in downstream enterprises, and their consumption attributes are strong. Small differences in essence and fragrances may cause huge changes in industry demand, so downstream manufacturers have high requirements for product quality and weak bargaining power. The pattern of supply side monopolistic competition ensures exclusive supply of patented formulas, and the market supply side has strong bargaining power. Therefore, in the pattern of strong supply and weak downstream, essence and spice industry leaders can maintain a high level of gross profit.

国内市场:行业集中度尚低,平均规模较小

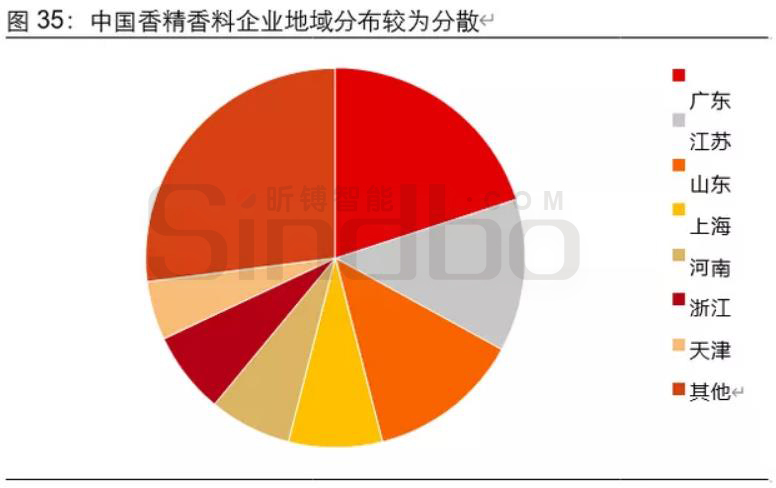

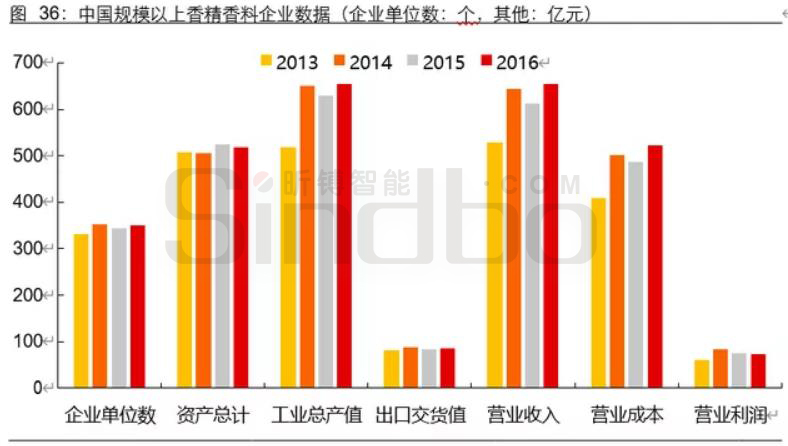

The production is rapidly increasing, and the supply pattern is relatively scattered. In the past 20 years, China's food industry, beverage industry, tobacco industry and other related industries have developed rapidly, as well as the innovation of related synthesis, extraction and flavor mixing technologies. The quality of essence and flavor products in China has continued to improve, the variety has continued to increase, the scale of enterprises has continued to expand, and the output and sales of products have increased year by year. There are a large number of essence and spice enterprises in China, with more than 1000 existing production enterprises, which are mainly distributed in Guangdong, Jiangsu and Shandong, with a low overall concentration. Among them, there are more than 300 enterprises above the designated size. In 2016, the average asset size was only 150 million yuan, and the average operating income was only 190 million yuan. The profitability of enterprises above the designated size is weak, the asset size is small, and the competitive advantage of enterprises is not obvious, forming a certain competitive advantage in the field of bulk essence and fragrance and the competition is fierce.

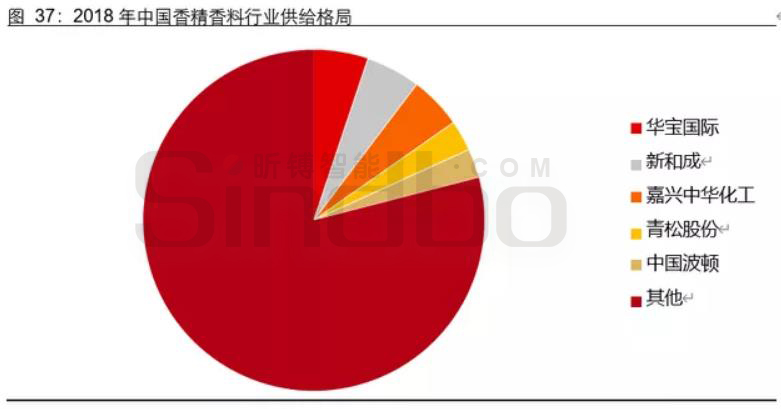

The concentration of industry supply is relatively low, and leading companies have significant room for improvement. Compared with foreign countries, the concentration of essence and fragrance industry in China is relatively low. In 2018, the CR5 of China's essence and fragrance industry was only 21.2% (estimated by the market share of the top five companies with operating revenue, without considering the market share of foreign companies in China), and the concentration was still low compared with the pattern of foreign oligopoly. In the future, driven by the tightening of domestic food additive control, the rise of environmental barriers, and the upgrading of domestic consumption, the survival space of small enterprises will be squeezed, and there is still a high room for improvement in the market share of leading enterprises.

The concentration of industry supply is relatively low, and leading companies have significant room for improvement. Compared with foreign countries, the concentration of essence and fragrance industry in China is relatively low. In 2018, the CR5 of China's essence and fragrance industry was only 21.2% (estimated by the market share of the top five companies with operating revenue, without considering the market share of foreign companies in China), and the concentration was still low compared with the pattern of foreign oligopoly. In the future, driven by the tightening of domestic food additive control, the rise of environmental barriers, and the upgrading of domestic consumption, the survival space of small enterprises will be squeezed, and there is still a high room for improvement in the market share of leading enterprises.

Food safety, environmental protection tightening, and consumption upgrading lead to industry clustering

The trend of food safety: stricter regulation and increased barriers to certification. In the future, as the industry standards and the management of additives become increasingly strict, downstream customers' requirements for the quality of essence and flavor products will also gradually increase, and the certification barriers of related industries will also gradually increase. Some small essence and fragrance enterprises have less R&D investment, poor product quality, or are difficult to pass the food verification. The requirements for food safety standards on the demand side have been raised, and leading enterprises have the financial and technological strength, which is expected to increase market share.

The trend of environmentally friendly production: policies are becoming stricter, and small businesses are accelerating their exit. In order to promote the construction of ecological civilization, national environmental protection policies continue to tighten. Since the first round of environmental inspections and "looking back" from 2016 to 2018, over 200000 chemical enterprises in China have been shut down in accordance with the law. Starting from 2019, in 2020 and 2021, the Ministry of Ecology and Environment will conduct a second round of inspections on the inspected objects over a period of three years. Utilize the year 2022 to conduct a 'look back' on some places and departments. There are a large number of essence and fragrance enterprises in China, with a wide geographical distribution and a small investment scale. Some flavor production processes involve more reaction processes and by-products, which pose a greater risk of environmental protection production. With the gradual pressure of domestic environmental protection policies, small essence and spice enterprises will withdraw from the market, and industry concentration is expected to increase.

The trend of consumption upgrading: quality improvement, new products seizing the market. With the improvement of people's living standards, consumers' consumption concepts for food and daily chemical products are becoming increasingly rational and mature, and their requirements for the quality of consumer goods are gradually increasing. Downstream consumers began to pursue safe, natural and environmentally friendly essence and fragrance products. In the future, essence and spice enterprises that master the research and development capability of new varieties are expected to launch more safe and reliable essence and spice varieties, meet the escalating consumption demand and increase market share.

Looking ahead, domestic food safety, environmental standards, and consumer upgrades will significantly increase the competitive barriers in the industry supply. Small businesses will find it more difficult to pass customer quality verification, national environmental approval, and customer brand selection, facing the risk of exiting the market, and the supply side is expected to clear. The domestic leading enterprises of essence and fragrance have capital and technical advantages, and the market share is expected to gradually increase.

Import substitution: R&D opens the way, high-end products are expected to break through

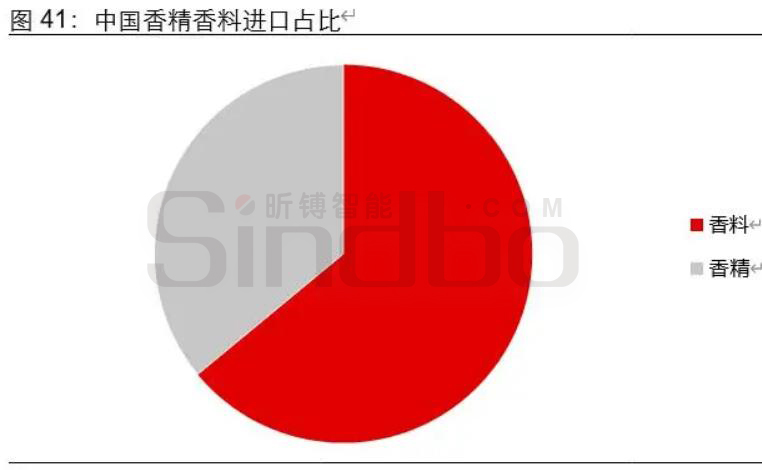

Imports are relatively concentrated, mainly in Germany and India. In 2018, China's imports of essence and spices were about 1.8 billion dollars, and the top five countries in terms of imports were Germany, India, the United States, Japan and Singapore. Compared with China's essence and spice export regions, the importing countries are relatively concentrated, and the sum of the top five imports accounts for about 70% of China's total imports of essence and spice commodities. China mainly imports synthetic spices from Germany, and essence accounts for a relatively small proportion. China mainly imports natural spices such as menthol and peppermint oil from India.

The import volume of menthol is relatively large, and the domestic market space is vast. From the perspective of imported products, the largest imported spice product in China is menthol, with an import volume of 12000 tons in 2017 and an average import unit price of 16.4 US dollars per kilogram. This is mainly due to the lower production cost of menthol in India and other places, which has a certain cost advantage. Secondly, the import volume of orange oil, benzaldehyde, and benzyl alcohol is over 1000 tons; There are also some high-end spice products in small batches (Turkic ketone, Rose ether, Macrostanone, high-quality dihydrojasmonate methyl ester), with small batch sizes and high added value, which cannot be produced by domestic enterprises and need to be imported from abroad.

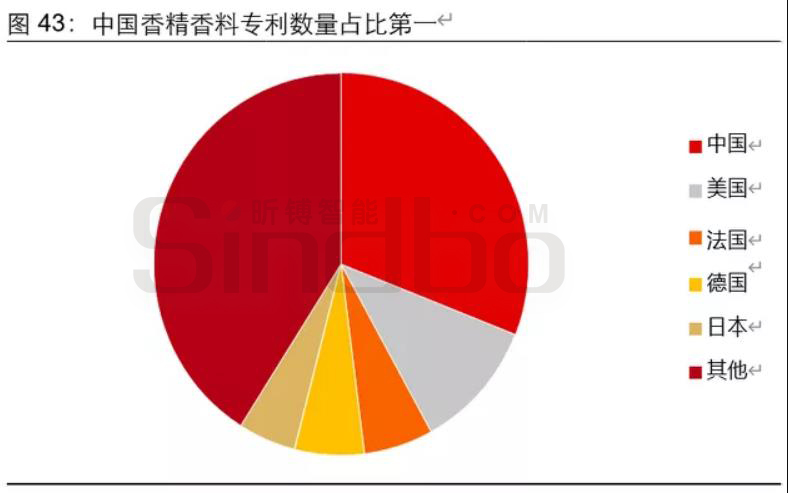

Domestic leading enterprises are accelerating their research and development layout, which is expected to replace imported high-end products. Compared with foreign essence and fragrance giants Chiwharton and IFF, the R&D investment of essence and fragrance enterprises in China accounts for a low proportion of operating revenue, and the absolute value of R&D investment is small. There is still room for improvement in the investment layout of R&D end. In the future, powerful essence and fragrance enterprises in China are gradually rising and strengthening R&D investment. In the past 30 years, China has ranked first in the number of essence and fragrance patents registered internationally, accounting for 31%, followed by the United States, accounting for 11%. At present, synthetic spice enterprises in China have broken through various new synthetic spice products such as cooling agent WS-23, carvone, methyl dihydrojasmonate, and furanone, while natural spice enterprises benefit from China's natural resource endowment and have certain market discourse power in various products such as osmanthus essential oil, litsea seed oil, and pine resin. China is gradually establishing a competitive advantage and is expected to gradually break through foreign monopoly products and achieve partial product import substitution.

On the supply side, overseas markets are in a highly monopolistic stage, and leading enterprises are laying out differentiated products to ensure competitive advantages. The concentration of supply in the domestic market is relatively low, and the average scale is small. In the future, under the combined effect of domestic food safety standards, environmental protection standards, and the improvement of consumption levels, the competition barriers in the industry will increase. Small enterprises without technological and financial advantages are expected to exit the market, and the industry is expected to move towards top concentration. At the same time, domestic essence and spice enterprises are gradually distributing related high-end essence and spice products, which is expected to break through the high-end product field and realize import substitution. The domestic essence and fragrance industry is facing a "golden age" of head concentration and import substitution, and domestic leading enterprises are expected to gradually increase their market share and strengthen their competitive advantages.

Looking forward to the future, the domestic essence and spice market is facing a high growth momentum, and the consumption attribute is gradually strengthened, with certain growth potential. On the supply side, large spice enterprises are gradually laying out high-end spice products, which is expected to form strong patent barriers, squeeze out market share of small enterprises, replace imported products, increase market share, and endow leading enterprises with internal growth potential.

Tel:

Tel:

Phone:

Phone:

Email:

Email:

Addr:

Addr:

Follow:

Follow: